In our most recent blog, we talked about three tax strategies that can help reduce your 2024 tax bill if you start focusing on them now, and we are bringing one of those strategies to life in this short case study. We hope you learn two things: how individualized your tax strategy should be, and that your portfolio can be a key resource in implementing your tax strategy.

Our case study focuses on identifying a tax desert, which is the BFS Advisory Group proprietary process to look ahead into our clients’ financial futures to see where tax rates will drop significantly for a short period of time – usually not more than a few years. As an example, business owners commonly experience a tax desert the year after they sell their companies – when they have no income and tend to be flush with cash.

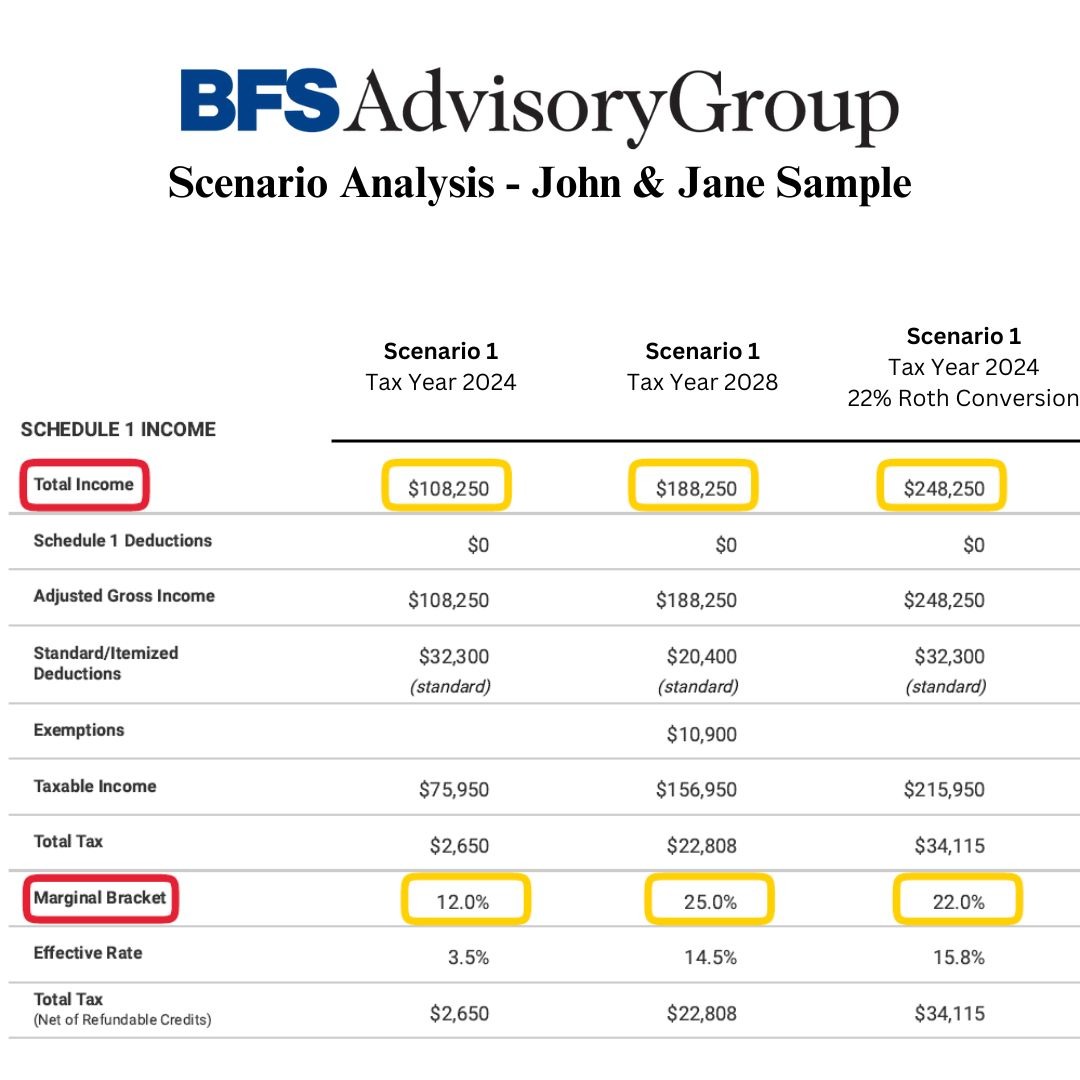

Another type of tax desert materializes when a married couple enters retirement prior to the age for Required Minimum Distributions (RMDs). In this scenario, a couple receives $70,000 per year in dividend and interest income, and $45,000 per year from Social Security benefits. The 2024 marginal tax rate for this couple is 12%.

Now, let’s look out four years to 2028, when this couple will need to begin RMDs and expects to withdraw $80,000 from their IRAs to satisfy their RMDs. The 2017 Tax Cuts and Jobs Act tax rates are set to sunset in the year 2026, bringing these clients to an expected marginal tax rate of 25% when they begin RMDs. What we see in 2024 and 2025 before those tax rates are set to expire is a tax desert – years where tax rates are projected to be lower before increasing again in later years.

Using this tax desert, we analyze various strategies that these clients can implement, from maximizing their current 12% tax bracket to increasing their opportunity with a tax bracket fill-up at the next rate of 22%.

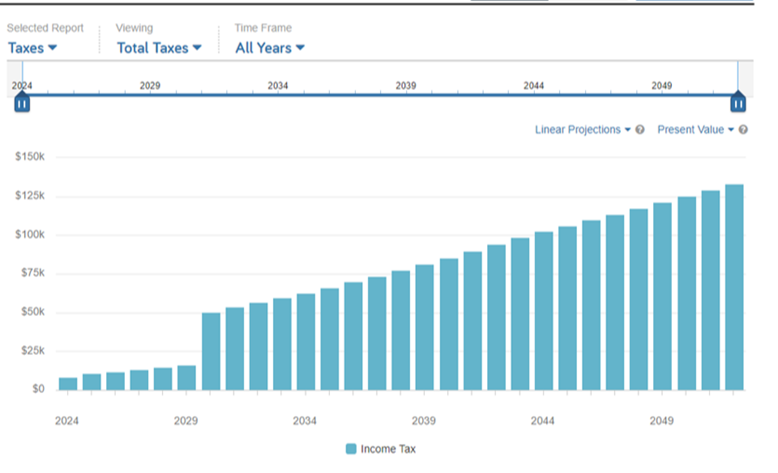

This couple could perform a Roth conversion of $140,000 in the year 2024, staying in a marginal tax rate of only 22%! At a hypothetical 8% growth rate, that $140,000 Roth IRA would grow to $300,000 within 10 years, all tax-free. Furthermore, that $140,000 conversion also reduces the IRA balance that would be subject to future RMDs. Our last step in our design process is to show our clients the multi-decade effect this type of tax strategy will have on the lifetime taxes they will pay.

Every year presents opportunities for you to implement tax strategies in your financial plan. If you need a review of your plan or portfolio for ways that you can reduce your own taxes or the taxes you pass on the next generation, contact us at hello@bfsadvisorygroup.com.

Debra Brennan Tagg is a CERTIFIED FINANCIAL PLANNER™ Professional and the creator of the DBT360 Financial Plan, a proprietary program that helps her clients prioritize their goals, leverage their resources, and address their risks. She is the president of BFS Advisory Group and teaches the public and the financial services industry about the importance of values-based financial planning and investor education.